Is there really a crisis in arts funding?

There's a perception in the sector that arts and culture funding is in crisis following largescale cuts in government funding and a perceived shift in emphasis for trusts & foundations to stem the tide of social welfare cuts. But is this true? And what's the future for arts & culture funding?

“England's arts face bloodiest cull in half a century as funds are cut for 200 groups” screamed the headline in The Guardian in December 2007, while editorials feared that the Conservatives' continued cuts could reduce the country's arts “to a national joke”. 2010 saw the Arts Council England budget cut by nearly 30%, and it was announced in 2012 that a further £11.6 million would be cut by 2015, with DCMS (the Department for Culture, Media and Sport) taking a further 1% cut in 2013/14 followed by 2% in 2014/15. The Government was accused of indifference towards the arts and of doing “next to nothing” to encourage greater philanthropy, by Nicholas Hytner, the then Director of the National Theatre.

The last ‘official’ figures on funding for the arts come from the 2011/12 Arts & Business Private Investment in Culture Survey, which has been monitoring this sector for the last thirty years[1]. This shows that in 2011/12 investment from local and national Government[2] made up just over two-fifths (41%) of the total income of the arts in the UK (see Figure 1).

Figure 1: The proportion of arts & culture funding provided by public and private investment and earned income (2011/12)[3]

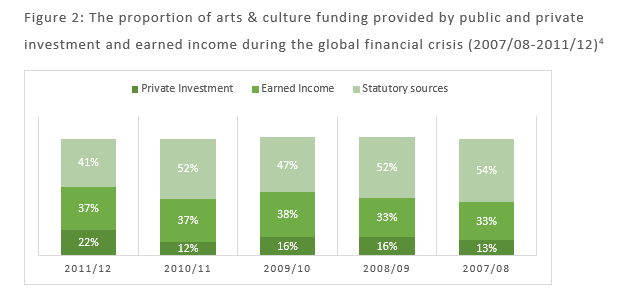

Looking at the long-term trends in arts funding shows how this has changed dramatically since the beginning of the global financial crisis (see Figure 2). Despite ups and downs, the proportion of state funding has declined from over half (54%) in 2006/07 to two-fifths (41%) in 2011/12; while correspondingly, the proportion of arts funding coming from private investment (individuals, companies and grant-making trusts and foundations) has increased from 13% to 22%, and earned income has increased from 33% to 37%.

Figure 2: The proportion of arts & culture funding provided by public and private investment and earned income during the global financial crisis (2007/08-2011/12)[4]

What’s the position of arts funding since 2012?

The latest Charity Financials spotlight report on charity causes shows that of the top 5,000 registered charities in the UK, just over 9% are Culture & Heritage charities[5], 472 organisations. This ranks arts and culture as the third most populous cause in the top 5,000 after religion (14%) and education and training (10%). Culture & Heritage organisations generate the highest proportion (12.5%) of the total income of the top 5,000 (£5.8bn), and this income has increased by 19% since 2011/12 (compared to 15.4% for social welfare charities). In addition, the new Top 100 Fundraising Charities Report[6] shows that the charity which experienced the biggest growth in income over the past five years was The Art Fund, which grew its fundraising income by 255 per cent between 2009/10 and 2014/15.

According to the charity causes report, two-thirds (65%) of the top culture and heritage charities report some government funding, compared to 25% who report legacy funding. However, the report also found that Culture & Heritage charities generate the most charitable activity income, £2.1bn in 2014/15 (representing 14% of all income from this source). So in terms of mixed income generation Culture and Heritage organisations appear to be in a strong position.

Now that the economy is recovering from the global financial crisis it appears that the arts sector is also on the way to recovery. In 2015 the Chancellor George Osborne described the arts as “one of the best investments we can make as a nation”, declaring the relevant ROI as £250 raised for every £1 invested. The Government pledged that Arts Council England and national museums and galleries would not receive further cuts, and would continue to receive the same amount of cash funding over the next four years – approximately £10 million per annum (in real terms this means a 5% reduction).

So was it all a storm in a recessional teacup? Not necessarily. Local authority funding is uncertain and further localised cuts will probably be forthcoming leading to new fears about a North-South divide in funding for the arts. Many regional museums and galleries are under threat from reduced funding and reduced footfall, as well as the fear of art being sold off to bring in cash. One in five regional museums were reported to be at least partly closed in 2015 according to a report by the Museums Association.

Should the arts be subsidised by public funding? Or, who should fund the arts?

There are those who argue that public funding stifles creativity, that corporate investment is charity-washing and that our great museums must remain free to enter. That doesn’t leave many options except individual donors and grant-making trusts and foundations; but with philanthropy gurus like Peter Singer telling us that private donors shouldn’t prioritise the arts over poverty-reduction, it’s unclear who’s responsibility it really is. This may be the arts sector’s real crisis.

[1] The Arts and Business Private Investment in Culture survey is based on an annual survey of arts organisations (sometimes supplemented by additional analysis of annual reports and accounts).

[2] The previous year’s survey suggests that lottery money makes up around 1.5% of this.

[3] Figures courtesy of The Arts and Business Private Investment in Culture survey.

[4] Figures courtesy of The Arts and Business Private Investment in Culture survey.

[5] Each organisation in the analysis has been assigned a single cause. Where an organisation could be placed in multiple causes, decisions have been made by Charity Financials on a case by case basis to apply a predominant cause. This is a highly subjective process and has quite an impact on the results, so this should be considered when reviewing the data.